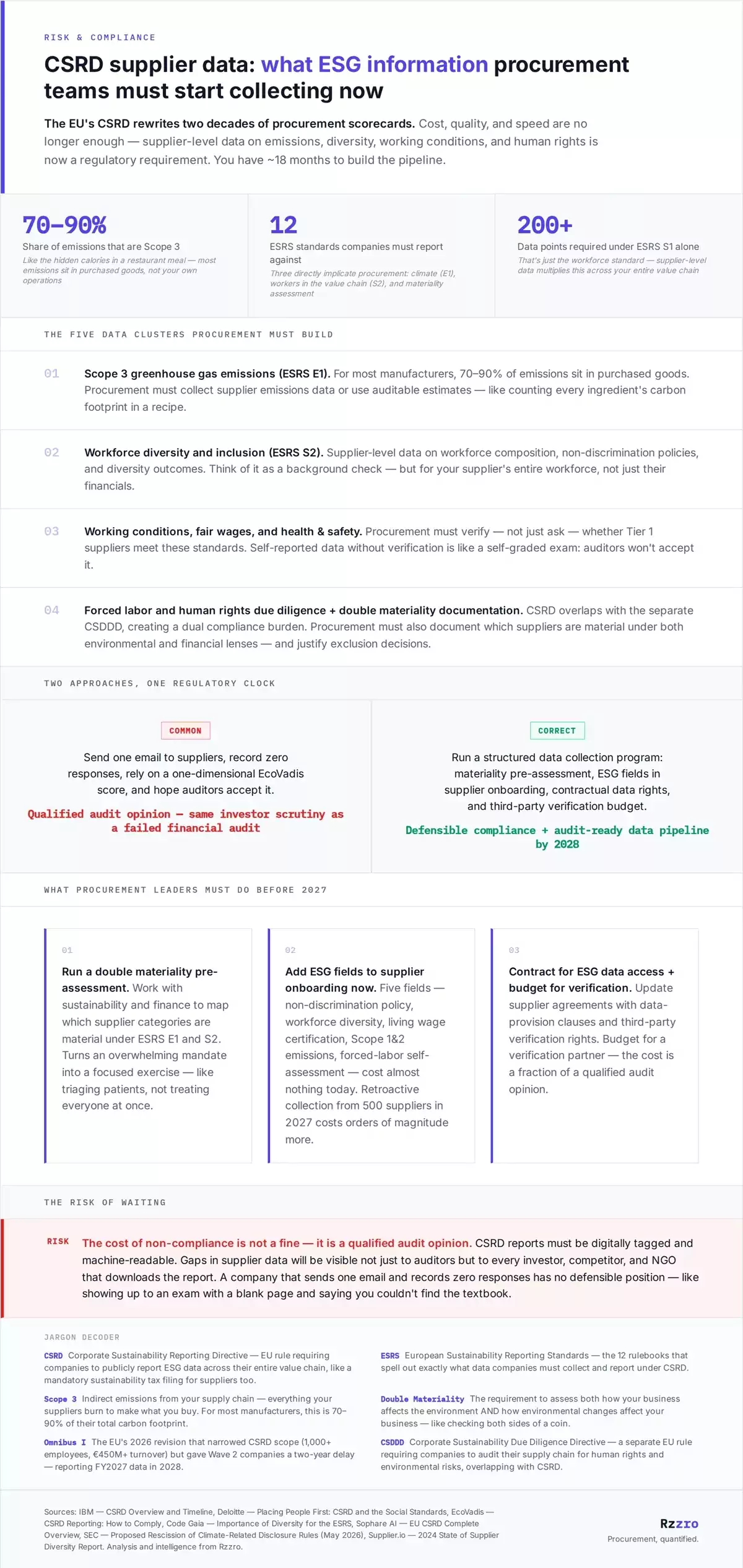

CSRD Corporate Sustainability Reporting Directive — EU rule requiring companies to publicly report ESG data across their entire value chain, like a mandatory sustainability tax filing for suppliers too.

ESRS European Sustainability Reporting Standards — the 12 rulebooks that spell out exactly what data companies must collect and report under CSRD.

Scope 3 Indirect emissions from your supply chain — everything your suppliers burn to make what you buy. For most manufacturers, this is 70–90% of their total carbon footprint.

Double Materiality The requirement to assess both how your business affects the environment AND how environmental changes affect your business — like checking both sides of a coin.

Omnibus I The EU's 2026 revision that narrowed CSRD scope (1,000+ employees, €450M+ turnover) but gave Wave 2 companies a two-year delay — reporting FY2027 data in 2028.

CSDDD Corporate Sustainability Due Diligence Directive — a separate EU rule requiring companies to audit their supply chain for human rights and environmental risks, overlapping with CSRD.

{kind=link}