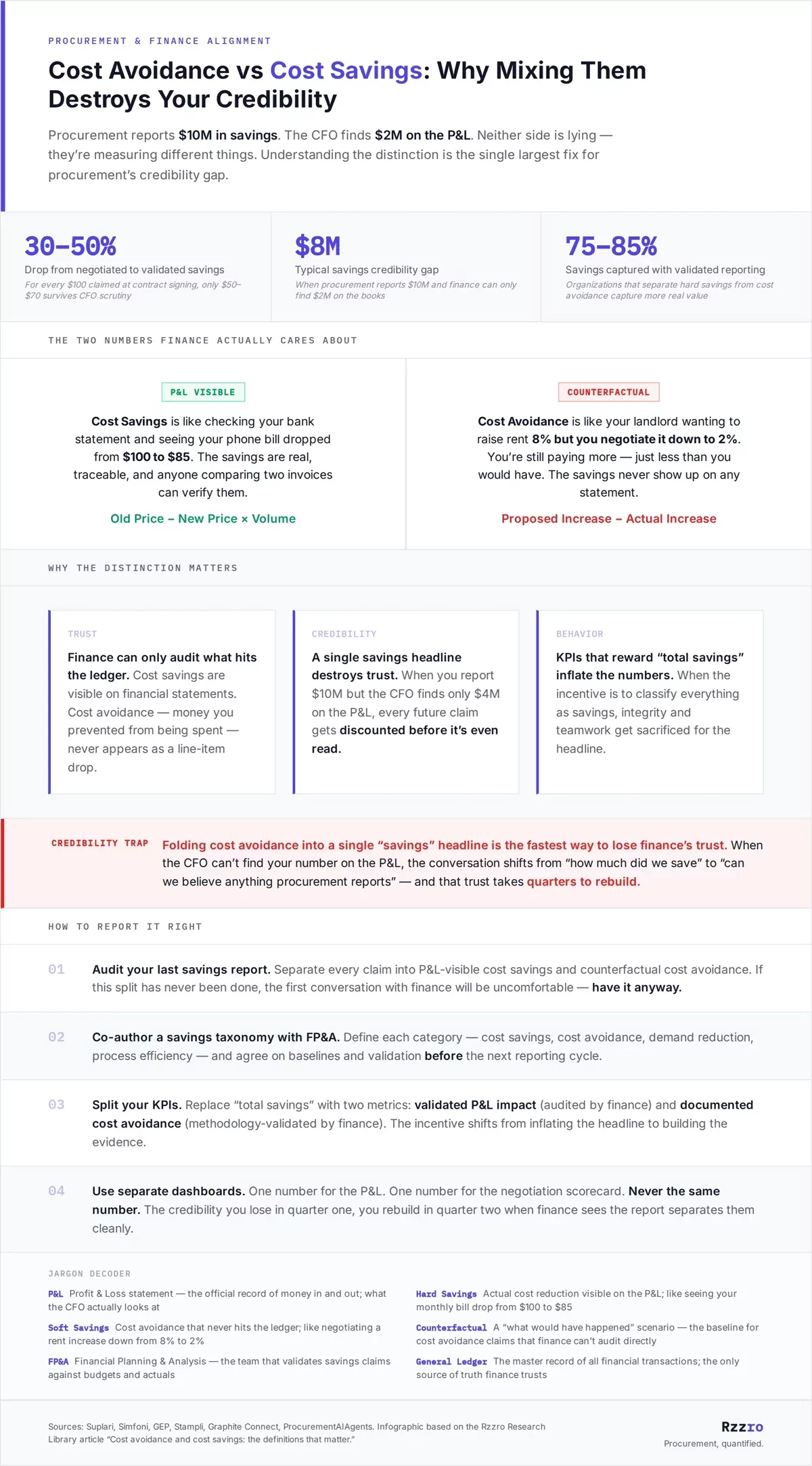

P&L Profit & Loss statement — the official record of money in and out; what the CFO actually looks at

Hard Savings Actual cost reduction visible on the P&L; like seeing your monthly bill drop from $100 to $85

Soft Savings Cost avoidance that never hits the ledger; like negotiating a rent increase down from 8% to 2%

Counterfactual A “what would have happened” scenario — the baseline for cost avoidance claims that finance can’t audit directly

FP&A Financial Planning & Analysis — the team that validates savings claims against budgets and actuals

General Ledger The master record of all financial transactions; the only source of truth finance trusts

{kind=link}