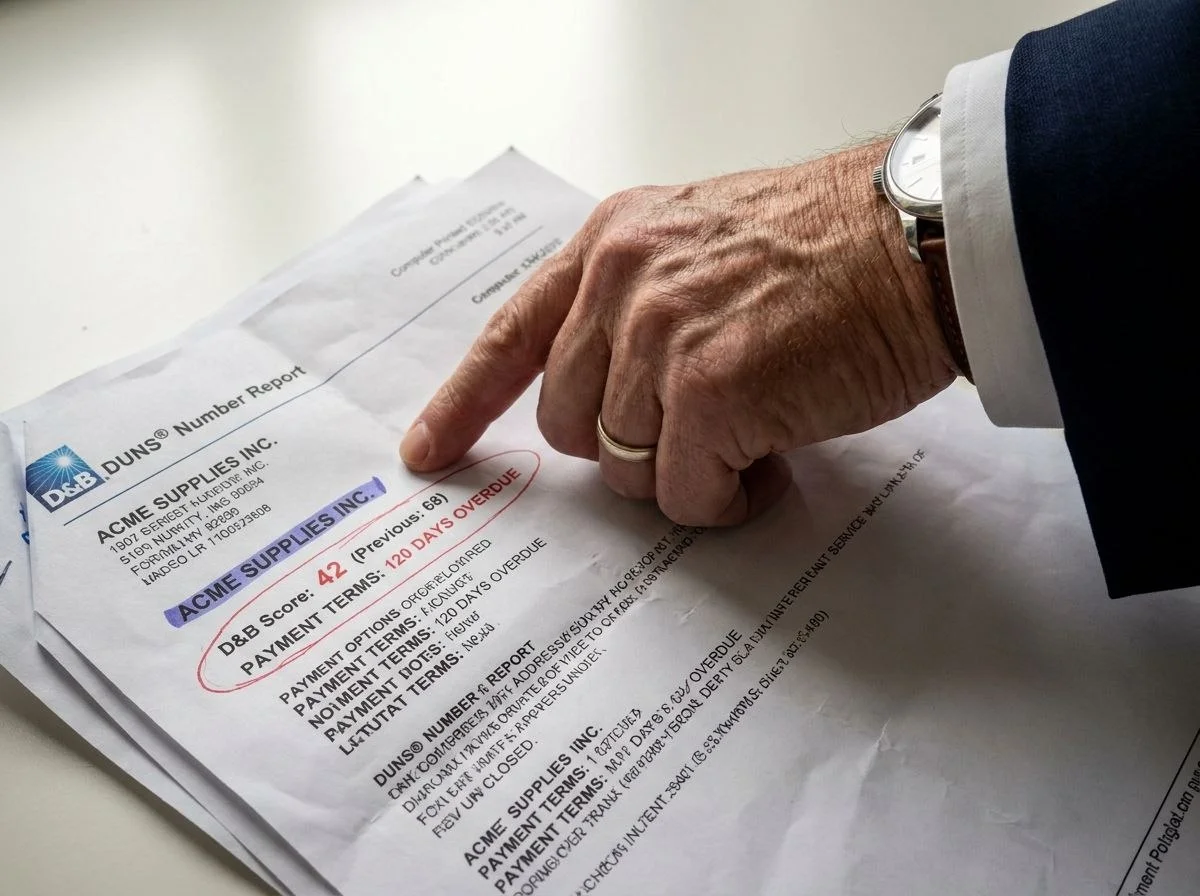

The warning signs were visible four months before the failure. Declining payment terms. Stretched deliveries. Quality issues escalating in frequency. But that intelligence was scattered across SAP, the procurement system, quality databases, and supplier emails — no single view existed .

This is not a hypothetical scenario. It is the pattern repeating across manufacturing and services supply chains in 2025-2026. Corporate bankruptcies hit a 14-year high in 2024 with 694 filings, continued rising through 2025, and public and private companies with over $100 million in assets filing increased 44% by mid-2025 . Chapter 11 filings reached a decade-long high in 2025 and are primed to continue into 2026 .

When was the last time you stress-tested your supply base against a tier-2 supplier bankruptcy? If the answer involves a spreadsheet and a manual email campaign, you have a problem that 2026 will expose.

The Hidden Risk in Your Supply Chain

Suppliers can "evaporate" without warning. In 2024-2025, business closures hit carriers like 10 Roads Express (affecting 2,500 trucks), Arnold Transportation (402 trucks), Kal Freight (800 trucks), and multiple others . These are not marginal players — they are established logistics providers that disappeared overnight.

The risk is concentrated in manufacturing and services sectors, which are heavily linked to complex supply chains and sub-tier suppliers . The elevated interest rates that drove this wave are not abating quickly — the Federal Reserve's measured easing cycle keeps borrowing costs relatively high, and tariff impacts are only beginning to appear in supplier financials .

The Early Warning Signals Your Data Already Contains

Predictive models can now forecast supplier failures 90-180 days in advance — if fed with the right data . The signals fall into four categories:

- Payment behavior and liquidity. Late or non-payment to creditors is a primary sign of stress. Deteriorating Days Payable Outstanding, repeated price-increase requests tied to "cash" or "credit" problems, and requests for shorter payment terms from you are all red flags .

- Operational performance degradation. Stretched deliveries and missed OTIF rates, with increasing frequency and variance, preceded a major supplier failure by months. Quality issues escalate alongside delivery slippage — a dual signal that is hard to ignore when viewed together .

- Financial and credit metrics. Z-scores, leverage ratios, interest coverage, credit-limit changes, covenant breaches, and rating downgrades are formal indicators. Regular collection and analysis of supplier financial reports is recommended practice .

- External macro overlays. Sector distress indicators (manufacturing, services), export-control or tariff exposure for tier-2/3 nodes, and concentration risk at single-source sub-tier suppliers all amplify bankruptcy probability .

The Cost of Blindness

Data-driven supply chain risk management approaches cut emergency procurement costs by 40-60% and reduce disruption costs by up to 50% through proactive planning . Firms using real-time control towers for visibility — expected to account for ~50% of large enterprises by 2025 — reduce logistics costs by ~15% and are first to react when a sub-tier bankruptcy hits .

When a flood strikes, a sub-tier supplier files for bankruptcy, or a cyberattack targets critical infrastructure, the first organizations to know are the first to act . The question every CPO must answer is: will your organization be among them?

Five Actions for the Next 90 Days

- Map your sub-tier dependencies. Identify critical parts, materials, and services down to tier-2 and tier-3. Flag single-point-of-failure components with no alternate source. In 2025, 22% of electronics delays were traced to a single specialized chip manufacturer with no backup .

- Build a composite risk score. Combine financial metrics (Z-scores, leverage), operational trends (OTIF deterioration), payment behavior, and concentration exposure into a single dashboard. Set thresholds that trigger automatic escalation .

- Embed financial health clauses in contracts. Require disclosure of covenant breaches, rating changes, and material litigations. Include audit rights for key tier-1 suppliers and their critical sub-suppliers .

- Formalize the procurement-credit partnership. Share financial distress intelligence between Procurement and Credit/Finance. Coordinate supplier support or exit strategies before a bankruptcy announcement forces your hand .

- De-risk through diversification. 67% of successful importers now diversify production across at least two geographic regions. Dual-sourcing coverage acts as insurance against sudden supplier failure .

The 2026 Imperative

Bankruptcy risk is not a tail event. With a 26% year-over-year increase in commercial filings and bankruptcy projections remaining elevated into 2026, supplier insolvency — especially at tier-2 and tier-3 — is a structural risk that demands a structural response .

The organizations that will navigate 2026 intact are those that have already moved from periodic supplier health checks to continuous monitoring. They have integrated financial, operational, and external data into a single early-warning system. They have mapped their sub-tier dependencies and diversified their critical sources.

Does your supplier risk function have a single view of financial health across your entire supply base — or are you still relying on spreadsheets and annual reviews to spot the next failure?